With it being the start of a new year, this is the best time to develop your 2022 financial plan. I have devised a 5-step financial planning checklist to kickstart your year.

This financial planning checklist will hopefully give you some ideas to help you make a game plan for your finances. I am NOT giving you financial advice – these are just financial tasks that I would personally do if I were beginning my financial-freedom journey.

Let’s kick off the new year on the right foot with these financial planning tips for 2022:

LEGAL DISCLAIMER: *The opinions expressed in the Professionally Peony are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the financial industry. The views reflected in the commentary are subject to change at any time without notice.

1. Set Your Financial Goals For The Year

Do you want to pay off a large sum of debt this year? Do you want to save for a down payment on a house? Are you trying to invest more money this year? Figure out what your goals are, and make a list of them.

Write your final, detailed and clear goal and then backtrack. What are the steps you need to take to reach this goal?

Example:

Goal: I want to pay off $10,000 of student debt this year

Steps I will need to take: Pay $833.33 every month toward my student loans using the avalanche method (make payments on each loan, while making the largest payment on the loan with the highest interest rate).

How I will be able to do this: I will use half the money I usually budget for fun spending and the other half from my miscellaneous spending budget. I will forego needless expenses to pay off my student loans

Maybe you want to start a side-hustle or look for passive income streams apart from your day job. Do your research on what you want to accomplish financially this year and how to begin the process. The hardest part of achieving any goal is just the task of getting started. JUST MAKE A SOLID PLAN GET TO WORK.

2. Build Your Buffer

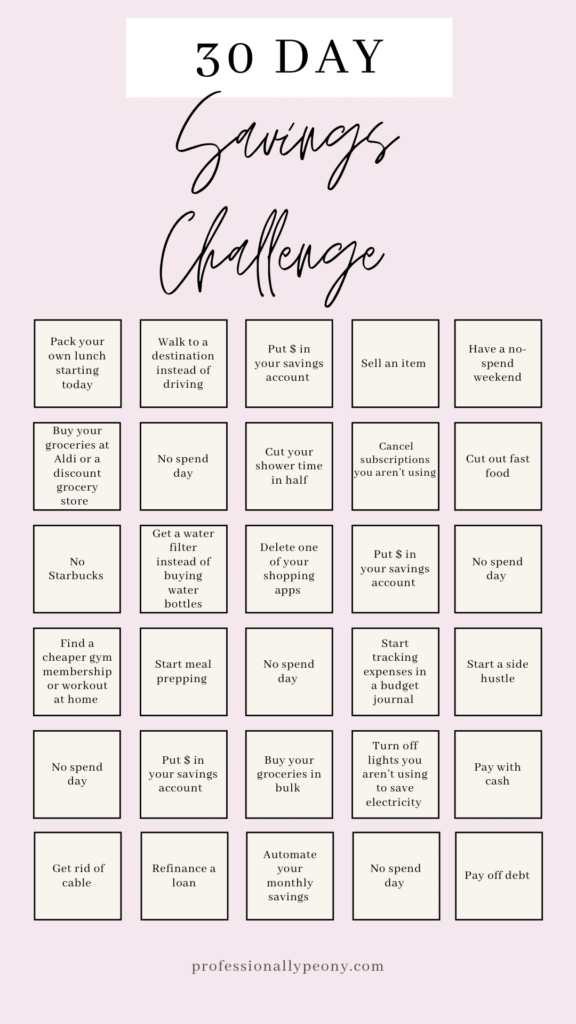

Start an emergency fund! An emergency fund can be any amount of money. Having $10 tucked away for a rainy day is better than having $0. In a time of crisis, it is crucial to have a buffer for an inconvenient expense.

A typical emergency fund should cover at least 3-6 months worth of your expenses, but only save as much as you feel comfortable with. You can have several different emergency funds, as well. I have two different emergency funds – one with a small sum of money for a rainy day, and the other fund covers several months worth of expenses.

Example:

Let’s say you get in a car wreck. You now have a $1,000 deductible you need to pay to fix your car.

Would you rather:

A) Be forced to use the money set aside for your bills and groceries to fix your car

B) Have to sell an investment or asset in order to get the $1,000

C) Have an emergency fund for times like these, so that you don’t have to worry about it

Answer choice “C” is hopefully what you chose. Having some money set aside to take care of unexpected expenses will save you a great deal of stress.

3. Consider Opening A Savings Account

I have an entire post on why and how to open a high-yield savings account here.

The gist is that a high-yield savings account is a better place to store your cash and savings because these accounts yield higher interest rates than checking accounts. Thus, you will be able to make more interest, faster off of your saved money.

If you aren’t 100% comfortable with opening a high-yield savings account, you still have the option to open a regular savings account (i.e., your local Wells Fargo savings account). Wherever you choose to save your money is completely up to you, but just remember that a regular savings account does not earn as much interest as a high-yield savings account.

The most important aspect of this financial planning checklist task is to SAVE SOME MONEY. Wherever you choose to save it.

4. Think About Opening A Brokerage Account

A brokerage account is simply just an investment account that allows you to invest in anything that you want. You can buy, sell, and trade securities on behalf of a company, investor, bank, or custodian. There is no tax on your investments until you SELL the investment for a gain, or you receive a dividend.

Brokerage accounts are much easier to access than retirement accounts since they are more of a short-term vehicle. You can save investments short-term or long-term, depending on your goals.

There are so many different brokerage accounts (Charles Schwab, Fidelity, Vanguard, Ally, ETrade, Ameritrade, Merrill Edge, and many more.)

Definitely consider looking into a brokerage account if you wish to invest some of your money.

5. Develop Your Budget

A budget consists of four items: income, expenses, savings, and investments.

Check out some great budget planning tips here and don’t miss the 3 best budgeting tools that you can find here!

Income:

Income is all money coming into your accounts. Figure out your post-tax annual income: I use this website here to determine my post-tax annual income, and then I divide it by 12 to determine my monthly income.

Add any extra income you receive each month (business interest, dividends, side-hustle income, rental property income, tax return income, etc.) and that is your monthly income

Expenses:

Expenses include rent, mortgage payments, debt, groceries, bills, and miscellaneous things you spend your money on each month.

Your expenses should ALWAYS be less than your income. You should aim to have more money coming in than going out.

Savings:

However much you wish to save per month should be allotted in your monthly budget. You can choose to save in a savings account, high-yield savings account, emergency fund, or sinking fund. Some people choose to save their money in their mattress (I would not recommend), but hey – to each their own.

Investments:

There is a place in your budget to decide how much of your income (if any) you wish to invest.

RELATED POST: [The Revised 50 30 20 Budget Plan]

6. Build Upon Your Financial Literacy

The best way to prepare yourself for financial success is to expand your knowledge of Finance itself.

Read as many financial literacy books as you can, listen to podcasts on financial topics you’re interested in, and even speak with someone who actually works in Finance. The greatest investment you could ever make is in yourself.

I have so many posts that are designed to help increase your financial literacy, so this blog is a perfect place to turn to!

[RELATED POST: THE 7 BEST PERSONAL FINANCE APPS THAT EVERY PROFESSIONAL NEEDS]

These were the 6 steps of my financial planning checklist for 2022. I hope this checklist helps you with your planning this year and encourages you to get in touch with your inner budgeter. As always, please email me if you have any questions at professionallypeony@yahoo.com!

Xo,

Layton

[…] [RELATED POST: THE 6 STEP FINANCIAL PLANNING CHECKLIST TO CRUSH YOUR 2022 GOALS] […]