Diving head-first into the world of Finance can be overwhelming. There are so many financial terms, lingo, and formulas that is becomes confusing. Financial Planning should be simple and make sense to you. You can’t control your finances if you don’t understand them.

I have devised a 5-step Financial Planning process for beginners so that you can have a nice place to start managing your money. I tried to make it as easy-to-follow as possible (not everyone has a degree in Finance!).

Please feel free to email me at professionallypeony@yahoo.com or DM me on Pinterest if you have any questions.

These are the 5 Financial planning steps for beginners!

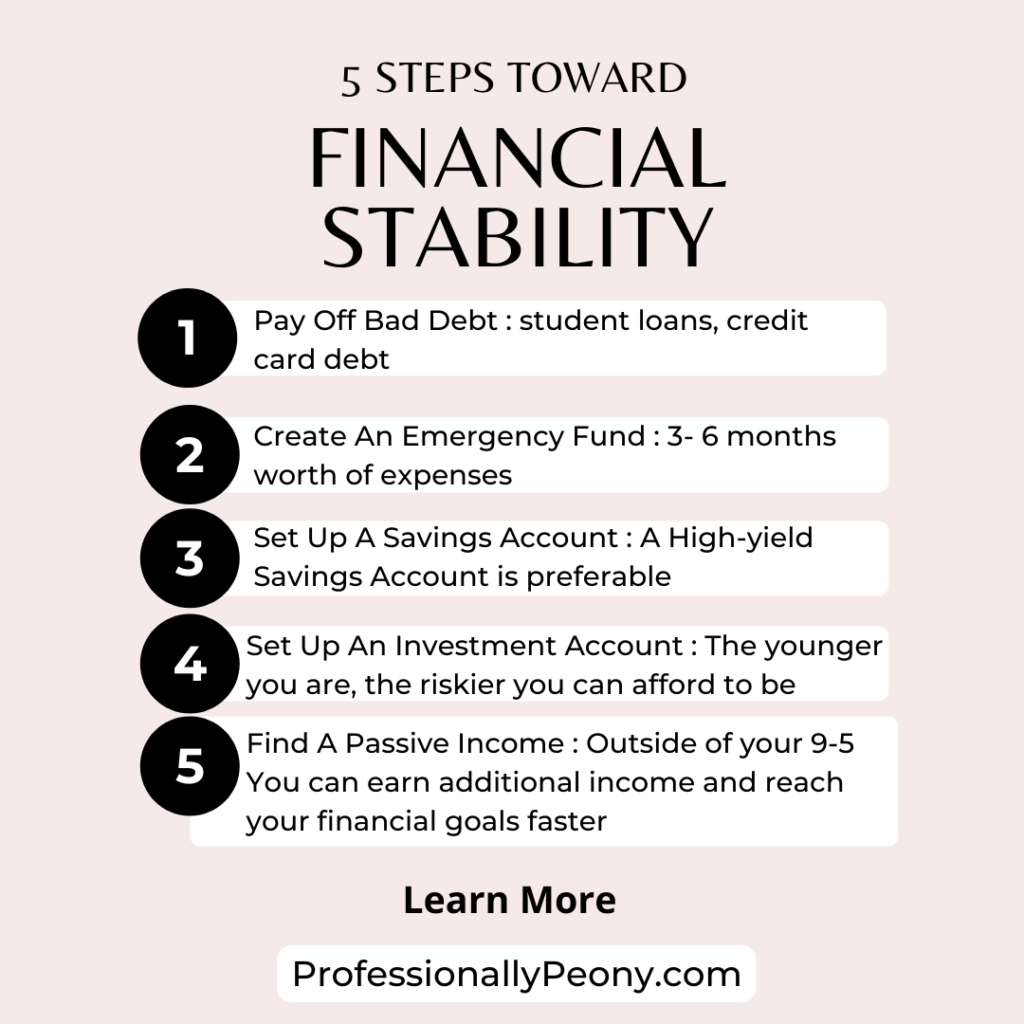

1. Pay Off Bad Debt

Bad debt is NOT your mortgage. Bad debt is the credit card debt, auto loans, and student loans. These are the debts that drain your income through crazy-high interest and monthly payments.

Unlike paying a mortgage on an appreciating asset (a house) that increases your net worth, your student loans dwindling your net worth.

Find a payment plan that works best for you. Avoid making minimum payments. The faster you pay off this bad debt, the less interest you will have to pay in the long run!

More on paying off student loans HERE

2. Create An Emergency Fund

An emergency fund is just a portion of your money set aside in case of an emergency (you lose your job, your house floods, your car breaks down, etc.)

The ideal amount to have saved in your emergency fund is 3-6 months worth of your required expenses. These expenses include rent, food, mortgage payments, utilities, and necessary healthcare items.

Having an emergency fund builds a financial buffer between you and any major life event that could get in the way of your financial goals.

Wouldn’t you rather have an emergency fund to tap into when something goes wrong than having to pull the money from your future down payment, wedding, or vacation savings? Failing to plan is a plan to fail!

3. Open A Savings Account

The financial rule of thumb is to put about 20% of your monthly income into savings. Obviously, you can put more or less into your savings depending on your financial well-being and goals.

The two main types of savings account are your standard savings account and a high-yield savings account. A standard savings account is just your run-of-the-mill Wells Fargo (or other bank) savings account.

The standard savings accounts earn virtually 0% interest on your money, but it is still better than hiding your savings under your mattress. Banks pay you to trust them enough to keep your money in their accounts, so they pay you a small interest on a tiny percent of your money.

A high-yield savings account is “high-yield” because it earns a higher interest on your money. Basically, you get more “free” money when you keep your savings in a high-yield savings account.

Whichever savings account you choose to keep your money in is completely up to you, but having a savings account is very important.

4. Open An Investment Account

Investing can seem scary, but the benefits usually outweigh the risks. Definitely do your research before you dive into anything. My biggest tips for first-time investors is to do your homework and start small.

I wouldn’t recommend throwing all of your money into Cryptocurrency if you are just learning how to invest your money.

I have so many posts on investing for beginners!

5. Develop A Passive Income Stream

Passive income is the systematic income you receive for something other than your main job. You receive earned income from working at a job.

Relying only on your earned income won’t build your wealth the same way having more than one income stream would. There are so many different side hustles you can do from your home that can bring in some extra money.

Here are some examples of passive income streams:

- Start a business

- Write a book

- Freelance work

- Tutor

- Rent out your house/condo

Find ways to make money outside of your job, and you will reach your financial goals faster.

These were 5 financial planning steps for beginners! I hope you learned something new 🙂

Xo,

Layton